Canadians today are having to spend the highest share of their disposable incomes on mortgage payments since the early-’90s, when the market was reeling from a collapse in prices.

That may lead some to speculate history is about to repeat itself, but a Hot Charts report from National Bank notes a key difference this time around.

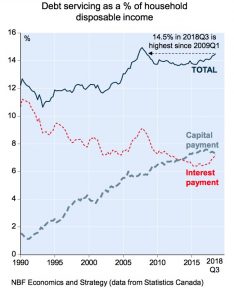

“Back in the early 1990’s, interest accounted for the bulk of mortgage payments. But as today’s Hot Charts show, capital repayments now account for almost half of mortgage payments,” writes Krishen Rangasamy, a senior economist at National Bank.

The upshot is borrowers are building equity, and therefore in a better position to shoulder shocks.

“That’s not to say we’re complacent about downside risks to the Canadian economy,” Rangasamy adds, noting higher debt servicing, rising interest rates, and fading real estate wealth are expected to hinder economic growth next year.

The National Bank report came on the heels of the publication of Statistics Canada’s third quarter national balance sheet and financial flow accounts.

According to the national statistical agency, Canadians are directing 14.5 percent of household disposable incomes towards debt servicing, which includes both interest and principal payments.

“Blame higher borrowing costs for this increase because interest payments now account for 7.2% of disposable income, a multi-year high,” says Rangasamy.

Total mortgage loans owed by borrowers in Canada declined by $1.2 billion, representing the third quarterly decline in a row.

Here’s Why Canada’s Appetite for Mortgage Debt Doesn’t Signal Another Housing Crash by Josh Sherman | Livabl

Recent Comments