Canadian Real Estate Association (CREA) kicked off 2026 with a headline that felt convenient : home sales fell 5.8% month-over-month in January, largely due to a “historic winter storm” in Central Canada.

But here’s the problem.

If it was just a snowstorm, it wouldn’t look like this.

The Numbers Don’t Point to Weather

January’s national data tells a very different story :

• Sales : down 5.8% month-over-month

• Sales : -16.2% year-over-year

• New Listings : +7.3% month-over-month

• HPI : – 0.9% month-over-month

• HPI : – 4.9% year-over-year

• Average Price : $652,941 (-2.6% YoY)

Weather doesn’t explain a 16.2% year-over-year decline. Snowstorms don’t cause national deterioration across provinces. And they certainly don’t cause sellers across two-thirds of markets to suddenly rush inventory onto the market.

If anything, January looked less like suppressed activity, and a lot more like a structural shift that we should start getting used to. It feels slow when you compare it to the “new normal” market we thought we created during the pandemic. But the truth is that we’re actually just back to an “old normal” market. Slow, steady :

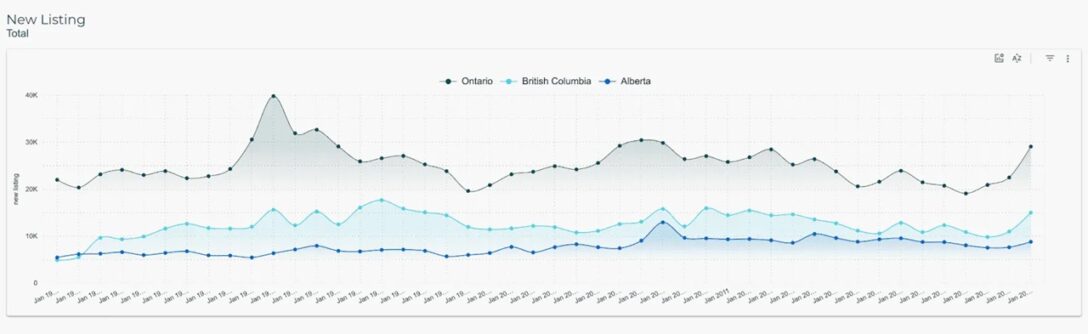

Supply is Rising. Demand is Hesitating

Supply is Rising. Demand is Hesitating

New listings jumped 7.3% in one month. That’s not subtle. Sellers certainly aren’t impacted by the snowstorms :

More importantly, that surge wasn’t isolated to Ontario. It was led by :

More importantly, that surge wasn’t isolated to Ontario. It was led by :

• Montreal

• Quebec City

• Calgary

• Greater Vancouver

• Victoria

Meanwhile, activity declined nationally while supply increased broadly.

That’s not weather. That’s leverage shifting.

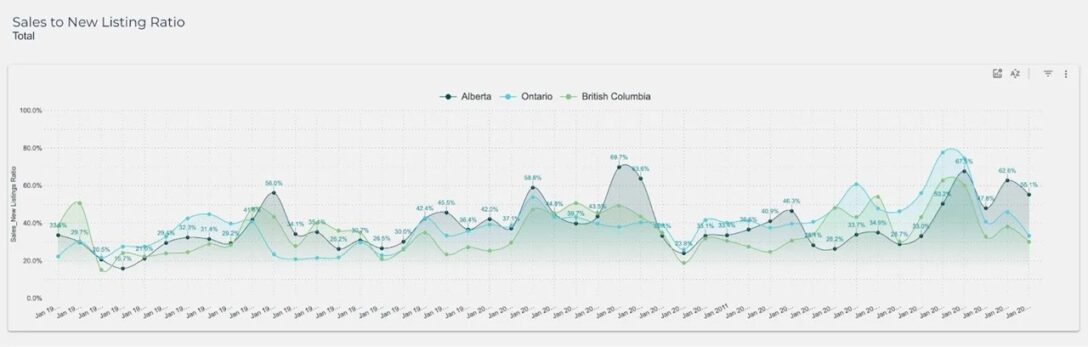

The sales-to-new listings ratio dropped sharply to 45%, down from 51.3% at the end of 2025. The long-term average is 54.8%. Balanced market territory sits between 45% and 65%.

We’re now sitting at the very bottom of “balanced” and bordering buyer’s market conditions.

And when markets tip toward buyers, price discovery follows.

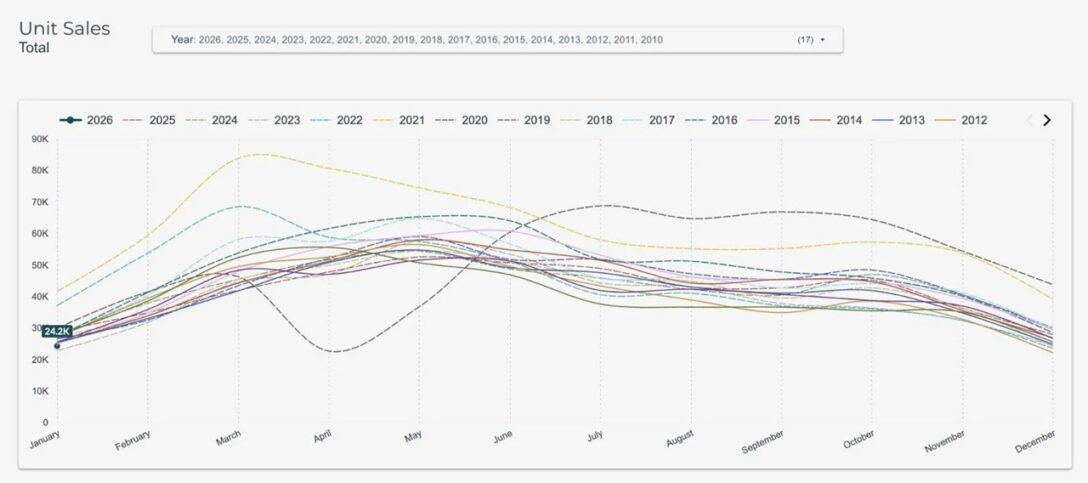

Inventory is climbing toward normal, but momentum is negative.

Inventory is climbing toward normal, but momentum is negative.

Months of inventory rose to 4.9 months, up from 4.6.

As mentioned, we’ve found an “old normal” market. Long-term average is about five months. A seller’s market is below 3.6 months and a buyer’s market would be above 6.4 months.

We’re not in a full buyer’s market yet, but behaviour already resembles one ..… and it’s felt that way for a year now. Housing markets are driven by momentum and psychology. When buyers believe they have time, they wait. When sellers sense hesitation, they compete. That’s exactly what January looked like. This is why economists fear deflation ..… it begets more deflation. If buyers see prices improving, they wait for prices to keep improving.

This is The Slow Grind Phase

There’s a misunderstanding about how housing downturns work. They don’t usually collapse in one dramatic move (unless rates spike violently, like 2022). Instead, the sequence looks like this :

1. Activity slows

2. Inventory builds

3. Price pressure follows

4. A long grind downward begins

We saw the sharp drop in 2022. What we’re seeing now is the grind.

The MLS Home Price Index fell 0.9% month-over-month in January. Annualized, that would imply a 10% to 12% decline — though monthly volatility shouldn’t be extrapolated too aggressively.

Year-over-year, prices are down 4.9%. From peak, the national average has fallen roughly 30%. That’s a massive erasure of equity for sellers, but a massive improvement of odds for buyers ..… so why are they still on the sidelines?

Regional Fragmentation, A Late-Cycle Pattern

Year-over-year price declines have now been visible in :

• British Columbia

• Alberta

• Ontario

• New Brunswick

• Nova Scotia

Meanwhile, smaller and more affordable markets like Sudbury, Quebec City, and St. John’s posted gains – affordability is the only thing that can stimulate markets. When peripheral, affordable markets outperform core urban centres, that often signals late-cycle dynamics. Capital retreats from high-beta, high-leverage markets first.

Ontario’s unemployment rate is sitting around seven per cent. Household leverage remains among the highest in the G7. Mortgage rates remain restrictive. Centimetres of snow don’t change that. We have a cycle to complete.

The “Pent-Up Demand” Question

CREA maintains that 2026 will ultimately be defined by pent-up demand from first-time buyers.

They may not be wrong ..… eventually.

But pent-up demand only matters if :

• Buyers qualify

• Buyers feel secure in their employment

• Buyers believe prices will rise

• Buyers feel urgency

Right now, affordability remains stretched. Income growth hasn’t materially accelerated. Investor activity is subdued outside government-insured multi-unit programs. Population growth has slowed sharply. And most importantly, buyers don’t feel urgency (nor should they).

Pent-up demand in theory doesn’t translate into transactions if buyers can’t qualify or don’t feel confident. And there’s just not really much to be confident about in Canada’s economy right now. Could that change once CUSMA is behind us later this year? Only time will tell ..… but I don’t see a point in getting too excited about it.

This Looks Less Like Snow and More Like Normalization

If you zoom out on the charts, something interesting appears. January 2026 doesn’t look like a collapse. It looks like normalization. For the last five years, we kept hearing about “new normal” everything. Real estate is bucking the trend and heading back to “old normal”.

Sales are around long-term averages. Inventory is near long-term averages. The sales-to-new listings ratio is weak relative to recent markets, but still within historical ranges.

What’s changed is the direction of travel.

We’re no longer in a post-pandemic scarcity market. We’re no longer in the “rates are zero, buy now or be priced out forever” phase.

We’re in a market where :

• Supply is meeting hesitation

• Buyers have leverage

• Price growth is capped

• Expectations are resetting

2026 : Worse Than 2025?

January came in significantly weaker than January 2025, and 2025 was already one of the slowest years on record in several major markets. Even if rate cuts arrive, they may arrive because economic conditions are deteriorating. And historically, people don’t aggressively lever up to buy homes during recessions.

As it stands, this is the second-slowest start to the year in the last 15 years.

The weather may have been cold, but the data suggests the slowdown runs deeper. The bigger question for 2026 isn’t whether snow delayed demand. It’s whether Canada’s housing market is finally transitioning from artificial scarcity to sustainable balance, and whether that balance requires lower prices before activity can truly recover.

The weather may have been cold, but the data suggests the slowdown runs deeper. The bigger question for 2026 isn’t whether snow delayed demand. It’s whether Canada’s housing market is finally transitioning from artificial scarcity to sustainable balance, and whether that balance requires lower prices before activity can truly recover.

Foch : After Five Years of “New Normal”, Housing Resets by Daniel Foch | REM Real Estate Magazine

Leave a Reply