Canadians may finally be getting skittish about real estate.

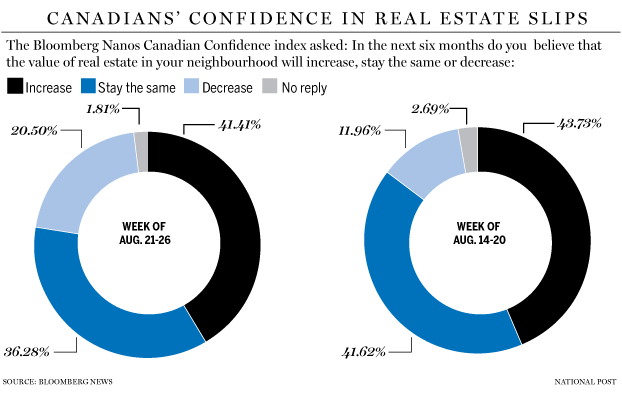

The share of survey respondents who expect a decline in local housing prices jumped by 8.5 percentage points, the most since weekly polling began three years ago for the Bloomberg Nanos Canadian Confidence Index. The increase to 20.5% from 12% dragged the broader sentiment index down from 2016 highs.

The reading marks a change from almost unbridled consumer optimism in a housing market that has carried the Canadian economy since the 2008 global financial crisis, even as policy makers warn price gains in some cities are unsustainable. Preliminary data this month from the Real Estate Board of Greater Vancouver show recent government measures to cool the market may be taking effect.

Countering the deterioration in housing market sentiment, the share of respondents who say their personal finances improved over the past year jumped 6 percentage points to 25.8%, also the largest increase since weekly polling began. The move coincides with government measures to increase monthly payments to lower-income families.

Prime Minister Justin Trudeau implemented the new child benefits as part of a program of deficit spending, with the first payments sent out last month.

“Cross-Pressured”

“Canadians are cross pressured –- on the one hand taking the newly changed Child Benefit but increasing concern about the value of real estate,” said Nanos Research Group Chairman Nik Nanos.

There’s no comparable increase in views that housing prices would fall since Nanos began gathering weekly data in May 2013. In the quarterly data preceding that, there was a jump of 24 percentage points at the end of 2008, just as the world financial system was melting down. That move was more than reversed two quarters later.

The share of those expecting home prices to rise or stay the same was more stable, while still downbeat. The 41.4% who see home prices rising was down from 43.7% in the prior week. Those seeing little change fell to 36.3% from 41.6%.

The shakeup follows British Columbia’s July decision to impose a 15% tax on Vancouver homes purchased by foreigners, effective Aug. 2. Average prices for detached homes in the city had surged to about $1.6 million, putting them out of reach of many local families.

“If there was to be a bit of a slowdown I don’t think it would be surprising given the strength that we’ve seen in the market over time,” Bank of Montreal Chief Financial Officer Tom Flynn said of the Vancouver market in an Aug. 23 phone interview. “We’re protecting ourselves from a risk perspective by having higher levels of equity down payments on more expensive properties, and we’ve been doing that for a period of time.”

To be sure, there are signs consumer confidence remains healthy. The Nanos Pocketbook measure rose to 62.5, the highest since February 2015. That helped keep the headline confidence measure of 59.3, close to the 2016 high of 59.9 set the week before.

Here are some of the other highlights from the report: Job prospects brightened, with the sixth straight increase in the share of respondents calling their positions “secure” to 50.4%; The confidence of people aged 40 to 49 rose to the highest since August 2014 at 60.1%; The economy will be little changed in six months according to 44.1% of those surveyed, up 2 percentage points from the prior tracking period; That was higher than the 26.5% who predicted strengthening and 23.2% who said it will be weaker.

The Bloomberg Nanos Canadian Confidence Index is based on a four-week rolling average of telephone polling with 1,000 respondents. It’s considered accurate within 3.1 percentage points, 19 times out of 20. The latest round of polling ended Aug. 26.

Canadians’ Confidence in Real Estate Juggernaut Starting to Wobble by Greg Quinn | Bloomberg News | Financial Post

Recent Comments