Canada Mortgage and Housing Corporation (CMHC) announced last week that it would raise homeowner mortgage loan insurance premiums effective March 17, charging borrowers “a few dollars more” every month. The rise will mean an increase of approximately $5 per month for the average CMHC-insured homebuyer, the corporation said. CMHC does not expect the higher premiums to have a “significant” impact on Canadians’ ability to buy a home. The changes will, on the other hand, “preserve competition in the mortgage loan insurance industry and contribute to financial stability.” Canada’s largest private mortgage insurer and CMHC’s main competitor, Genworth, announced identical premium changes. The changes do not affect those who already have mortgages, or who have applied for them.

The increased premiums will contribute to financial stability inasmuch as they will give CMHC more money. Since January 1, new capital requirements came into effect, requiring mortgage insurers to have more capital on hand as a buffer in case an economic shock were to cause mortgage defaults to increase.

There is also an argument that the higher premiums could act as a cooling mechanism in the housing market, making it a little less easy for first-time buyers to get in, which would eventually make prices more affordable. This contradicts CMHC’s own statement about the new rates having little significant effect on buyers. An increase of $5 a month does not seem likely to stop a would-be buyer from pursuing her dream.

Some have pointed out that in the Toronto market, where home prices are much higher than elsewhere, the average monthly increase is more likely to be somewhere between $10 and $15. Further, it must be remembered that over the life of the mortgage, the premium would be in the neighbourhood of $25,000. But would that smallish monthly increase deter buyers contemplating a mortgage of $700,000?

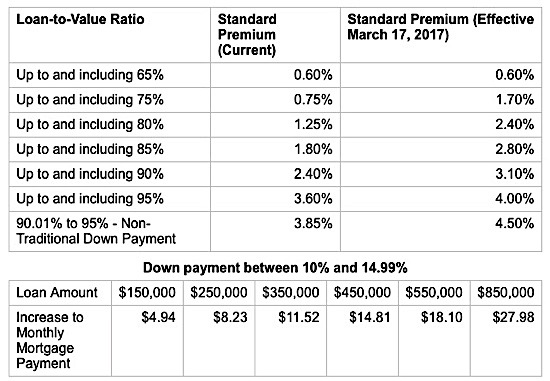

As it is, the new rates affect those with the least amount of money to start with. Everyone with less than a 20 per cent down payment must buy mortgage insurance, but those with the smallest down payments pay higher rates. So, a person putting down just 5% today would pay a premium of 3.6%. As of March 17, the same buyer will have to pay 4%.

In comparison, the premium for a mortgage with a loan-to-value ratio of 80% (a down payment of 20%) is currently 1.25%. It will rise to 2.4%. Depending on the size of the mortgage, that would mean a monthly increase of between $7.06 ($150,000) and $39.96.($850,000), based on a 5-year term at 2.94%.

According to CMHC, the vast majority of its loans are for less than $600,000 (95%) and about half are for less than $300,000. The average loan on CMHC’s books is about $245,000.

CMHC Mortgage Insurance Premium Hikes Not Likely to Affect Buyers by Josephine Nolan | Condo.ca

Recent Comments