The thing that is on all prospective home buyers’ minds before they start getting a mortgage is the down payment required to begin the process. According to Canadian regulations, you can not simply get a mortgage with no down payment amount towards the purchase price of the home.

This means you will need to save up at least some level of down payment before you are able to purchase real estate. Just how much you decide to, or are able to, save will depend on your own situation and the loan in question. This article will explain how minimum down payments work, how mortgage loan insurance affects how much you pay, and how much of a down payment is right for you.

Is a down payment a deposit?

A down payment should not be confused with a deposit. In terms of buying a home, a deposit is an amount of money that you have to provide to the seller along with your offer to buy a property. The purpose of this deposit is to prove that you are serious about buying and that you have the money to handle the related closing fees. Upon the sale of the home, you can put the deposit towards your down payment or towards the closing fees. Deposits are typically much smaller than down payments.

Your down payment is essentially the amount of the purchase price that you pay upfront. This means while it is not returned, it does get converted into an ownership stake in the property and its equity. Your down payment is important for your lender as they will have down payment requirements that determine your mortgage eligibility and rates.

Is there a minimum down payment?

There is a minimum amount of money you will be required to put down as a down payment. The amount of the minimum will depend on the purchase price of the property being acquired. Generally, the higher the purchase price, the higher the down payment percentage you will be required to pay.

Homes valued at $500,000 or less

For a home with a value of $500,000 or less, you will be required to put a minimum down payment of 5% of the purchase price.

Homes under $1 million

For a home with a value above $500,000 and up to $999,999, you will be required to pay a minimum down payment of 5% on the first $500,000 of the purchase price and then 10% on any amount above that. For example, if your home was valued at $750,000 and you wanted to make the minimum down payment, you would first pay 5% of $500,000, or $25,000, then you would pay 10% of $250,000, another $25,000. Your total minimum down payment would be $50,000, or about 6.6% of the total value.

Homes above $1 million

For a home with an assessed value above $1 million, the minimum down payment is a much steeper 20% of the value.

Remember, these are the legal minimums. That means that based on your own situation, the bank may require a larger down payment from you, but they will never allow you to pay lower than the minimum.

When you need to purchase mortgage default insurance

In order to protect Canadian mortgages from default, it’s required that for mortgages paying a down payment below 20% that the borrower also purchases mortgage default insurance, also known as mortgage loan insurance. Mortgage loan insurance offers no protection to you as the borrower but pays out to the lender in the event of you failing to meet payments. You may even be required to cover the costs of the payment going to the lender. Your lender may also require you to buy default insurance as a part of their mortgage terms, even with a down payment of 20% or more.

The price of your mortgage default insurance will depend on your loan to value ratio. The smaller your down payment, the higher the mortgage insurance premium will be. This can complicate the idea of a minimum down payment because though your down payment may be low, the effective amount of money you are paying is higher than that.

Example

For example, with CMHC insurance, a 5% down payment is required to purchase mortgage loan insurance at a rate of 4% of the total home value. In some provinces, you will also pay provincial sales tax on your insurance. That means your 5% down payment will actually cost you about 9%.

Luckily, mortgage insurance does not need to be paid in a lump sum (though that is an option). Instead, you can add it to your mortgage principal and pay it through your monthly mortgage payments. However, you will now pay interest on the value of your insurance, meaning more interest paid overtime, and possibly a higher monthly payment.

Your mortgage loan insurance payment, along with your mortgage rates, is why it is not always the best idea to go for the lowest possible down payment, as you can end up paying a lot more in the long run.

Is there a maximum down payment?

There is technically no maximum down payment you can put on a mortgage, in fact, you can buy a home outright if you wanted to. You should actually aim to pay as high as is realistic for you, as it will reduce the amount of debt you hold.

The thing is that for most people saving a sizable down payment takes long enough, and saving more money than needed is not really in your interest. Consider the cost of living while you are saving for a down payment. If you spend decades saving for a large down payment, you could have used a smaller down payment to secure a mortgage and pay into your home’s value instead of paying rent.

There are some cases where a larger down payment is beneficial, however, such as if you have a poor credit history and the lender is wary of giving you a loan.

What is the normal amount to put down on a house?

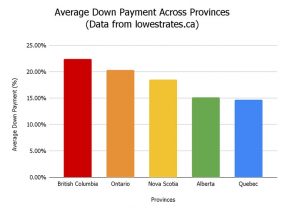

The average down payment that Canadians pay varies a lot by region, as home prices, household incomes, and market conditions, can all affect the amount one chooses to pay. The Canada real estate and housing market report from lowestrates.ca presents their recent findings from mortgage data in 5 of Canada’s provinces. Here’s what they found.

Canadians generally opt for high down payments

Generally, though there are options for lower payments, Canadians prefer to pay larger amounts whenever possible. In British Columbia, people paid the highest average down payment amount at 22.45%. Based on the average home price, that means a payment of almost $160,000.

Ontarians paid the second-highest average down payments at 20.35%. People from Nova Scotia paid 18.54% on average, while Alberta and Quebec paid 15.15% and 14.68% respectively.

How much should I put down?

Generally, the more you can put down the better. A higher down payment can reduce or eliminate the burden of mortgage default insurance. In addition, it will allow you to get better mortgage rates from your lender, and pay less on your monthly mortgage payment. Overall, you will save a lot of money if you are able to put up a large down payment.

If you aren’t able to save up such a large amount, or you are eager to get into your home as soon as possible, there is nothing wrong with paying a lower down payment. It is just important that you inform yourself of the impacts it will have on your mortgage and make sure it is financially worth it for you.

Conclusion

Hopefully, we have helped you figure out what your down payment influences your mortgage, and how much of a down payment works for you. Now that you have the info it’s time to start saving your down payment fund. If you want to learn more about the nitty-gritty of mortgages, check out some of our other guides on mortgage interest, affordability, or our 2022 mortgage rate forecast.

What is The Average Down Payment on A House in Canada and How Much Should You Pay? by Corben Grant | Canadian Real Estate Wealth

Recent Comments